Understanding Life Insurance Loans Benefits, Drawbacks, and Considerations Life insurance is a vital financial tool that provides financial protection to individuals and their families. It offers a death benefit to heirs upon the insured’s death. still, life insurance programs frequently come with fresh benefits, similar to the capability to take out loans against the policy’s cash value. In this composition, we will claw into the generality of life insurance loans, exploring how they work, their advantages and disadvantages, and pivotal considerations when concluding analogous loans.

What’s a Life Insurance Loan?

A life insurance loan, also known as a policy loan, is a fiscal arrangement that allows policyholders to adopt plutocrats against the cash value of their endless life insurance programs. endless life insurance programs, similar to whole life and universal life insurance, accumulate a cash value over time. This cash value grows duty-remitted and can be penetrated through policy loans.

When a policyholder wants to take out a life insurance loan, they request a loan quantum from the insurance company, using the policy’s cash value as collateral. The insurance company determines the maximum loan quantum available grounded on the cash value and any outstanding loan balance. The policyholder can admit the loan proceeds in the form of a lump sum or regular inaugurations.

The loan is commonly subject to an interest rate, which is set by the insurance company. The interest rate may be fixed or variable, depending on the policy terms. The interest on the loan generally does not need to be paid outspoken but rather accrues over time. Policyholders have the inflexibility to repay the loan in colorful ways. They can choose to make regular loan disbursements, including interest, or they can let the interest accrue and repay the loan at an after date.

One of the primary advantages of a life insurance loan is that it provides policyholders with access to cash without the need for a credit check or lengthy blessing process. The loan quantum is generally available within a short period, making it an accessible option for individuals in need of immediate finances. also, since the loan is secured by the policy’s cash value, policyholders don’t need to suffer credit checks or meet specific credit qualifications.

Life insurance loans also offer inflexibility in terms of prepayment. Policyholders can choose a repayment schedule that suits their fiscal situation. They can make regular payments to gradationally repay the loan or let the loan interest accrue, reducing the immediate fiscal burden. still, it’s important to note that if the loan remains overdue, the interest can compound over time, potentially reducing the policy’s cash value and death benefit.

It’s pivotal to understand that taking out a life insurance loan has certain disadvantages as well. One significant disadvantage is that the loan quantum, along with any accrued interest, is subtracted from the policy’s death benefit. However, the outstanding balance can significantly reduce the quantum that heirs admit upon the insured’s death If the loan isn’t repaid. likewise, failing to repay the loan or maintain the policy adequately can result in the policy lapsing or being terminated, which may lead to the loss of the death benefit and any remaining cash value.

Before concluding on a life insurance loan, it’s important to precisely consider the purpose of the loan, develop a realistic repayment plan, and understand the implicit impact on the policy’s performance. Seeking guidance from a fiscal counsel or insurance professional can help policyholders make informed opinions and alleviate implicit pitfalls associated with life insurance loans.

How do Life Insurance Loans Work?

Life insurance loans work by allowing policyholders to adopt against the cash value of their endless life insurance programs. Then is a step-by-step breakdown of how these loans generally work

Cash Value Accumulation

Permanent life insurance programs, similar to whole life and universal life insurance, make up a cash value element over time. A portion of the decorations paid by the policyholder goes towards this cash value, which grows duty-remitted.

Loan Request

When a policyholder wants to take out a loan, they communicate with their insurance company and request a loan against their policy’s cash value. The insurance company will give the necessary forms and guidelines for initiating the loan process.

Loan Quantum Determination The insurance company determines the maximum loan quantum available grounded on the policy’s cash value and any outstanding loan balance. The specific loan-to-value rate and policy terms may vary depending on the insurance company and policy vittles.

Loan Terms and Interest Rates

The insurance company sets the interest rate for the loan, generally at a fixed rate. The interest rate may be lower than what’s available in the request since the loan is secured by the policy’s cash value. The policyholder should review and understand the loan terms, including the interest rate, repayment schedule, and any freights associated with the loan.

Loan Blessing and Disbursement

Once the policyholder accepts the loan terms, the insurance company reviews the request and approves the loan. The loan proceeds can be expended in the form of a lump sum or regular inaugurations, depending on the policyholder’s preference.

Prepayment Options

Policyholders have inflexibility in repaying the loan. They can choose to make regular loan payments, including both top and interest or conclude for interest-only payments. However, the loan interest may accrue and be added to the loan balance, potentially reducing the policy’s cash value, If the policyholder doesn’t make regular payments.

Impact on Death Benefit

When a policyholder takes out a life insurance loan, the loan quantum, along with any accrued interest, is subtracted from the policy’s death benefit. However, the outstanding balance is abated from the death benefit paid out to heirs, If the policyholder passes down before repaying the loan.

Loan Prepayment and Policy Conservation

It’s important for policyholders to repay the loan according to the agreed terms to avoid negative consequences. Failing to repay the loan can result in the policy lapsing or being terminated, which may lead to the loss of the death benefit and any remaining cash value.

Advantages of Life Insurance Loans

Access to Cash

Life insurance loans gives policyholders an accessible way to pierce finances without the need for a credit check or lengthy blessing process. The loan quantum is generally available within a short period.

No Credit Qualifications

Since the loan is secured by the policy’s cash value, policyholders don’t need to suffer credit checks or meet specific credit qualifications. This makes life insurance loans a charming option for individuals with lower-than-perfect credit.

Flexible Prepayment Options

Policyholders have the inflexibility to repay the loan on their terms. They can choose to make regular loan disbursements or let the loan interest accrue, reducing the immediate fiscal burden.

Duty Advantages

Life insurance loans are generally duty-free, meaning that policyholders don’t have to pay income duty on the loan quantum. still, it’s essential to consult a duty professional to understand the specific duty counteraccusations grounded on individual circumstances.

Disadvantages of Life Insurance Loans

Reduced Death Benefit

When a policyholder takes out a loan against their life insurance policy, the loan quantum, along with any accrued interest, is subtracted from the policy’s death benefit. However, the outstanding balance can significantly reduce the quantum that heirs admit upon the insured’s death If the loan isn’t repaid.

Accumulated Interest

Life insurance loans generally accrue interest, which can compound over time. However, the interest can eat into the policy’s cash value, potentially reducing its long-term growth, If the loan remains overdue.

Threat of Policy Lapse

Failing to repay the loan or maintain the policy adequately can result in the policy lapsing or being terminated. The policyholder may lose the death benefit and any remaining cash value if the loan balance exceeds the policy’s cash value.

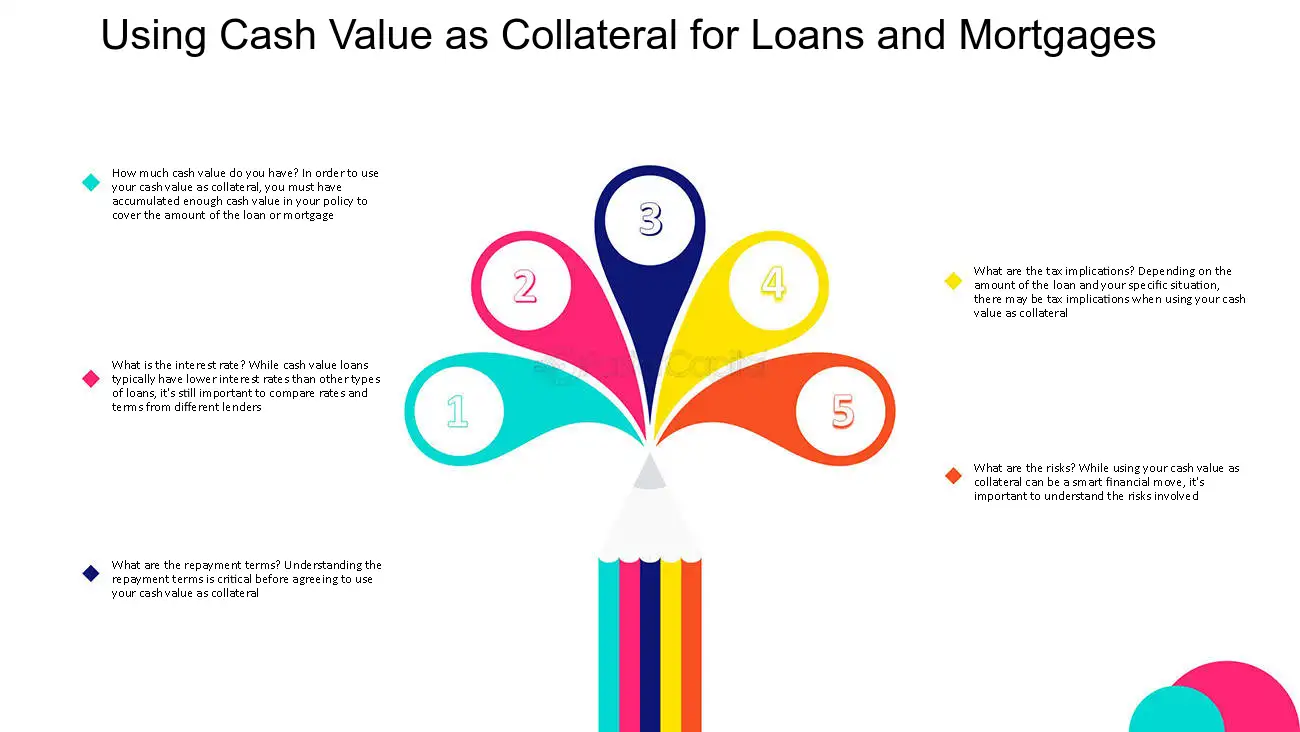

Considerations Before Taking a Life Insurance Loan

Purpose of the Loan

It’s pivotal to consider whether the loan is necessary and aligns with your fiscal pretensions. Life insurance loans should immaculately be used for essential charges, similar to exigency medical bills, education costs, or debt connection.

Loan Prepayment Plan

Developing a realistic prepayment plan is essential Failing to refund the loan can lead to adverse consequences, analogous as a reduced death benefit or policy lapse. estimate your fiscal situation and ensure you can comfortably meet the loan prepayment scores.

Impact on Policy Performance

Taking a loan against the policy’s cash value can affect the policy’s growth eventuality. It’s vital to understand how the loan and any accrued interest may impact the policy’s cash worth and death benefit over time.

Professional Guidance

Before making any opinions regarding life insurance loans, it’s judicious to consult with a fiscal counsel or insurance professional. They can give substantiated guidance predicated on your specific circumstances and help you make informed choices.

Conclusion

Life insurance loans can be a premium resource for policyholders in need of immediate finances. They offer quick access to cash without the need for credit qualifications. still, it’s essential to precisely consider the advantages and disadvantages before concluding on a life insurance loan. Understanding the impact on the policy’s cash value and death benefit, formulating a repayment plan, and seeking professional advice can help policyholders make informed opinions and palliate implicit risks. Flashback, life insurance programs are primarily designed to give fiscal protection to heirs, and exercising the cash value through loans should be approached with careful consideration of long-term counteraccusations.

{kind=link}